When a company transitions to being owned by an employee ownership trust (EOT), there are a number of changes to get used to.

Not least the fact, that the new circle of control gives employees as much power as a collective in an EOT as anyone else. And also your old boss is no longer invincible!

But beyond those, there are some significant other adjustments to make.

It is one of these changes that we will take a closer look at today, can an EOT pay dividends?

Let’s find out.

Can An EOT Pay Dividends?

When a company is employee-owned, the employees are eligible for profit share payments which are considered a cash bonus rather than a dividend. This means income tax is not payable on the first £3,600 of profit share per employee, per year. On top of this, these payments must be made by the trading company, not the EOT. Effectively this is done instead of the EOT itself receiving dividends.

What Are Dividends?

Before we tackle the main question, it is worth recapping what dividends are.

Dividends are simply a payment a limited company makes to its shareholders if it has made a profit.

So this is from the money remaining after paying all business expenses and liabilities and outstanding taxes.

It is a reward to the owners of the shares for investing in the company.

The word dividend comes from “dividendum” in Latin, which translates to “something to be divided”.

So How Does It Work in an EOT?

In short, an EOT doesn’t receive or pay dividends.

It will instead ask the trading company to process profit share payments to its employees via the trading company’s payroll, with what it might have otherwise received as a dividend from the trading company.

The EOT pays nothing directly.

So rather than being paid out to shareholders as dividends, profits can be shared with employees as a bonus.

The profit share payment must be applied equally, and on a “same terms” basis for all employees. That means individual employees cannot be favoured.

As long as the EOT owns a majority of the company, the first £3,600 of this profit share is tax-free per employee, per year (although National Insurance contributions are still payable).

Anything above this is subject to income tax as normal.

It’s all done via the payroll of the trading company, with things like NICs/student loan deductions, as well as tax on anything above £3,600, being dealt with there. Hence no need for employees to file self-assessment tax returns simply due to receiving this share of profits.

On the Subject of Dividends…

If you are considering transferring your business to your employees, it is worth remembering that there is zero capital gains tax payable on the sale proceeds of a business to an EOT.

Dividends on the other hand can suffer 39% or higher personal tax.

So if you are planning on selling to an EOT in the future, it can make sense to restrict your dividends to a modest level in the run-up to the sale, if you can afford to do so.

This is because the cash will build up in the company, and it will come to you tax-free immediately following the transfer.

And to answer another question business owners who are considering going EO often ask, if you continue to work for the company after you have sold it, then you are still entitled to a profit share payment.

There can be some confusion on this point. The key thing you’re not allowed to do is benefit from the onward sale of the business by the EOT. The reason being you’ve already benefitted from selling the business, so it seems unfair you can benefit again!

We have answered this and many other queries on our frequently asked questions page.

What About Hybrid Companies?

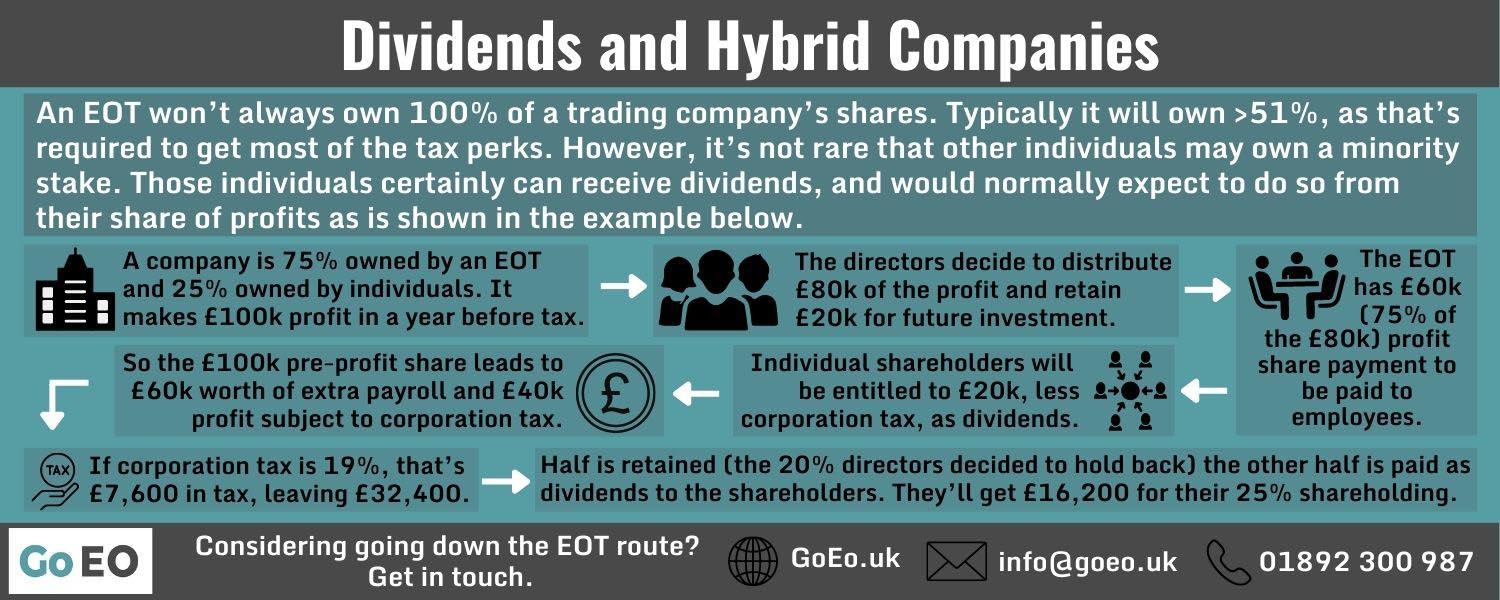

An EOT won’t always own 100% of a trading company’s shares. Typically it will own >51%, as that’s required to get most of the tax perks. However, it’s not rare that other individuals, perhaps senior employees, may own a minority stake.

Those individuals certainly can receive dividends, and would normally expect to do so from their share of profits.

Say for example a company is owned 75% by an EOT, and 25% by individuals, and in a given year it makes £100k profit before tax.

The directors would consider how much of that profit it wanted to distribute, vs retain for future investment. Let’s say they decide on 80% distribution, so £80k.

The EOT will then typically have a £60k (being 75% of the £80k) profit share payment, which it will instruct the trading company to pay out to employees. This will then be reduced by the employer’s NICs to establish how much is actually processed.

The individual shareholders will be entitled to £20k, less corporation tax, as dividends.

So in this situation, the £100k pre-profit share will lead to £60k worth of extra payroll, hence £40k profit left that’s subject to corporation tax.

If corporation tax is 19%, that’s £7,600 tax suffered, leaving £32,400 left.

Half of that is retained (being the 20% the directors decided to hold back), the other half is paid out as dividends to the individual shareholders.

So they’ll get £16,200 in this example, for their 25% shareholding.

Summary

In short, an EOT cannot pay/receive dividends for two reasons:

- Profit share payments are made to employees which are considered a cash bonus rather than a dividend. This is because it can be paid without the company having to make a profit or have distributable reserves.

- These payments must be paid by the trading company, not the EOT.

The fact that the profit share payments are considered a bonus, not a dividend, means income tax is not payable on the first £3,600 of profit share per employee, per year (although National Insurance contributions are still payable).

Anything above this is subject to income tax as normal.

Either way, it is definitely quite a perk!

If the EOT doesn’t own 100% of the shares, remember minority shareholders will be entitled to dividends on their share of profits.

If you are interested in finding out more about transitioning to an EOT, get in touch with us at Go EO to see how we can help.