On this page

- Can An EOT Be Sold?

- Selling an EOT: The Basic Considerations

- Selling an EOT: The Tax Considerations

- Tax Consideration: Capital Gains Tax

- Tax Consideration: Deferred Consideration

- Tax Consideration: Income Tax/NICs for Employees

- What About if an EOT Decides to Sell A Small Portion of its Shares?

- Summary

The question of whether an Employee Ownership Trust (EOT) business can be sold is interesting.

EOTs are a relatively new concept, at least in terms of mainstream UK adoption. So it isn’t something that has been explored particularly deeply yet.

But also because an EOT, as a trust, is nebulous, it is simply there to own the shares in the trading company.

So can you sell an EOT? Or what happens when an EOT sells its shares?

That is what we are going to look at today.

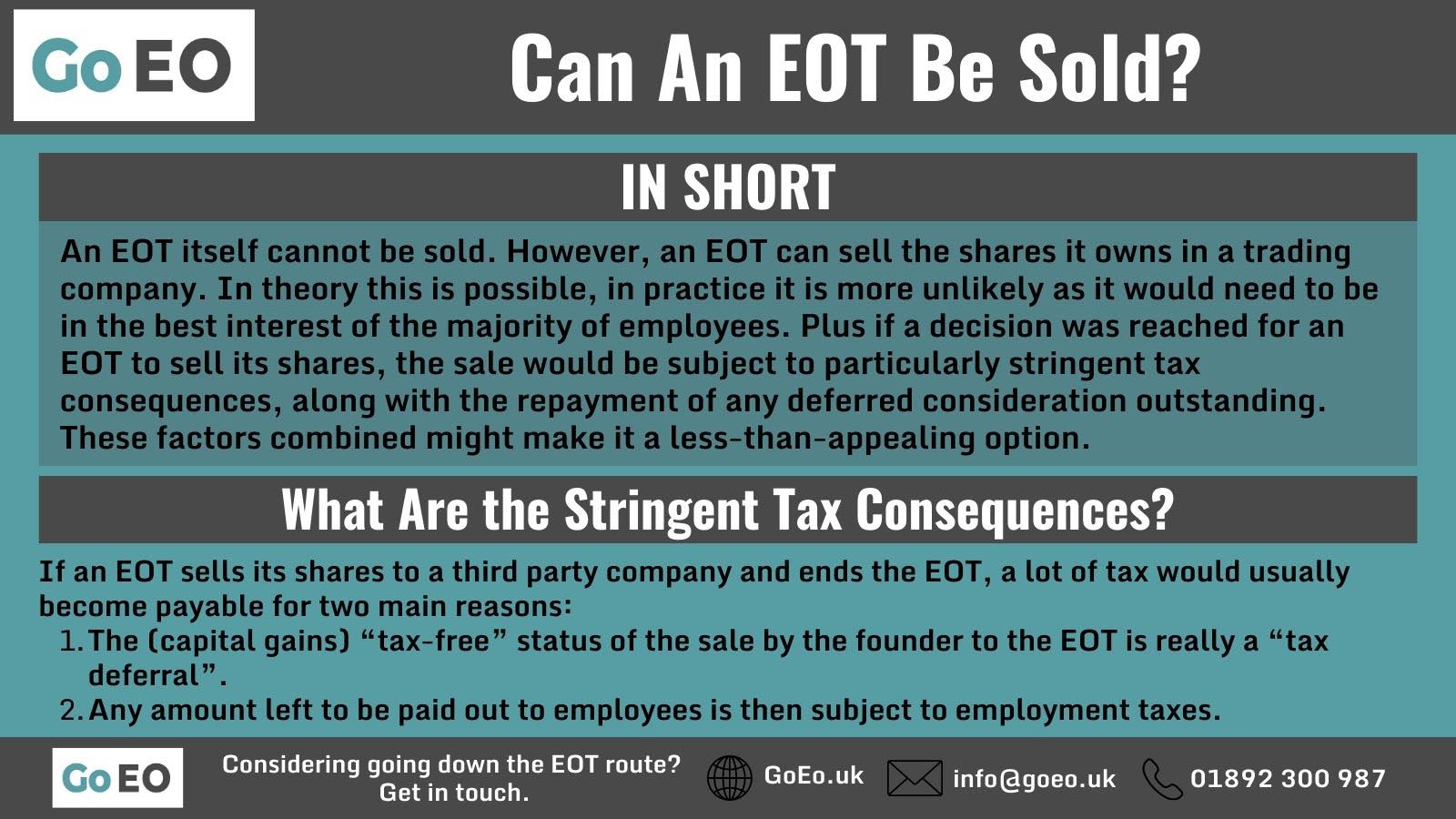

Can an EOT be sold?

An EOT itself cannot be sold. However, an EOT can sell the shares it owns in a trading company. In theory this is possible. In practice, it’s unlikely as it would need to be in the best interest of the majority of employees.

Plus if a decision was reached for an EOT to sell its shares, the sale would be subject to particularly stringent tax consequences, along with the repayment of any deferred consideration outstanding. These factors combined might make it a rarely appealing option.

Selling an EOT: The Basic Considerations

Let’s get the semantics out of the way first, strictly speaking, an EOT itself cannot be sold. That is because, as mentioned in the introduction, as an entity an EOT is somewhat nebulous.

But what can happen is an EOT can sell the shares it owns in a trading company. So when people ask if you can sell an EOT, they usually mean this.

So in theory this could happen, and an EOT can sell its shares. In practice, it is unlikely to happen.

A large reason for this is the unique structure of an EOT, which gives everyone a say in how the business is run.

For an EOT to sell its shares, it would need to be agreed amongst staff that it was the best option for the majority of the employees, now and in the future.

It couldn’t simply be a case of a few maverick staff deciding to go ahead and do it.

Then any potential buyer would most probably be nervous about a drop in productivity, as staff would no longer be incentivised by a profit-sharing payment, which could result in a drop in productivity.

Plus those staff would have just received a lump sum from the sale. So again, would they be happy to continue doing their best work for that business going forward?

Then on top of that, the pure financials have a few issues which can make it less appealing for the employees/trustees.

Let’s take a close look at this last point.

Selling an EOT: The Tax Considerations

Firstly, we’re going to assume the shares aren’t being sold to another EOT. This is potentially possible, and if it were to happen, none of the below applies. It would instead be considered another no gain no loss transfer.

Assuming the sale isn’t to another EOT but a third-party individual/company, it ends the EOT, and a lot of tax would typically become payable!

There are two main reasons for this:

- The (capital gains) “tax-free” status of the sale by the founder to the EOT is really a “tax deferral”.

- Any amount left to be paid out to employees is then subject to employment taxes.

Digging into these in a bit more detail.

Tax Consideration: Capital Gains Tax

When a founder sells their shares to the EOT, you may hear it’s tax-free. It effectively is, but in geeky terms it’s deemed a “no gain no loss transfer”. This is more commonly seen with married couples passing assets between them.

It means that whilst no tax is payable, the party receiving the asset inherits the base cost of the initial owner.

Also, that tax status is only on the basis the EOT meets all key criteria to qualify not just at the point of sale, but also at least until the end of the tax year after the tax year the sale happened.

Sounds a bit complex? A few examples to demonstrate it may help:

CGT Example 1

Joe Bloggs set up a Ltd Co on 1 July 2013, with 100 x £1 shares. That’s his initial investment in the company, £100.

Ten years later, Joe sells the business to an EOT for £1million on 30 June 2023. Joe’s gain would be the difference between £1million and £100, so £999,900. Due to the tax status of EOT sales, he pays zero capital gains tax.

However, one year later, on 30 June 2024, the EOT sold those shares on for £1.5million. From that date it therefore no longer controls the company.

Joe sold the business on 30 June 2023, in the tax year ending 5 April 2024. The end of the tax year after is therefore 5 April 2025.

As the EOT sold the company on 30 June 2024, it lost control before 5 April 2025. This is sufficient to negate Joe’s beneficial tax treatment on initial sale to the EOT.

Hence in this situation, whilst Joe’s sale to the EOT was eligible for no gain no loss treatment at the time it happened, actions afterwards mean this is clawed back. Joe’s historic sale becomes taxable, suffering capital gains tax based on £999,900 gain.

The EOT then suffers capital gains tax just on its actual gain of £500,000 (the £1.5million less £1million it paid for the shares).

CGT Example 2

Joe Bloggs set up a Ltd Co on 1 July 2013 with 100 x £1 shares. That’s his initial investment in the company, £100.

Ten years later Joe sells the business to an EOT for £1million. Joe’s gain would be the difference between £1million and £100, so £999,900. Due to the tax status of EOT sales, he pays zero capital gains tax.

Again, the EOT sells the shares on, for £1.5million. All the same as example 1 so far.

However, this time the EOT sold the shares a year later than example 1, on 30 June 2025. As this was after the end of the tax year following tax year of sale, the founder’s beneficial tax status is not at risk.

The whole CGT liability sits with the EOT. It inherits the initial base cost of Joe. So whilst it sold for £500,000 more than it paid to buy the shares, it’ll be taxed on a much larger gain of £1,499,900.

The trust has to pay capital gains tax based on the gain as if it initially set the company up for £100. It can’t claim anything back from the founder with respect to this. The tax rate for trusts is generally 20%.

You’ll perhaps note the total amount that suffers capital gains tax is the same in both example 1 and example 2. The difference is who pays it. In example 1 Joe suffers ~2/3 of it, the EOT just ~1/3. In example 2, the EOT suffers all of it.

CGT Example 3

It’s worth bearing in mind that if things went badly, the EOT might sell the shares for less than it bought them for. Even in this situation of making a loss on sale, it can still have to pay capital gains tax.

For example, using similar numbers as before, the founder set up the company for £100. The EOT buys it for £1million.

Over the next five years, business isn’t great. The EOT eventually sells the shares for £600,000. Just 60% of what it paid for the shares.

Despite making a £400,000 loss, it would still pay capital gains tax based on a £599,900 gain.

Tax Consideration: Deferred Consideration

Whilst obviously not a tax, we’re adding this section in here due to the order these things would need paying.

The EOT will pay capital gains tax based on whatever the sales price was, less the appropriate purchase price (which may be the founder’s initial set up share capital only).

If the EOT still owes money to the founders based on the sale to the EOT, this would then need to be settled in full.

This is similar to if you buy a house with a mortgage, pay off a little bit over a few years, then sell the house. Inevitably you need to clear the balance of the mortgage before you can enjoy what’s left.

Tax Consideration: Income Tax/NICs for Employees

Ok, so capital gains tax has been paid on the sale, and the founder has had any amounts remaining owed to them cleared off. Fingers crossed there’s still something left. What next?

Finally the employees can receive this, hurrah!

It will typically be apportioned like a profit share payment. So individuals can’t be positively or negatively discriminated against. It might be split evenly across everyone. Or potentially split in line with salary etc.

It’s worth mentioning that any participators are specifically excluded from receiving this amount.

For instance if the founder still worked in the business at the time the EOT sold the shares, the founder wouldn’t be able to receive a share of those proceeds.

Any non-participator employees are then taxed on the proceeds left as employment income.

This means income tax at their marginal rate. As it can (hopefully) be a big sum, this can mean even those on a very average wage can be pushed into higher/additional rate bands.

It also suffers national insurance, plus potentially things like student loan repayments etc too.

Each individual’s loss to tax will therefore vary significantly depending on their own personal circumstances, but often the employment taxes can be 50+% of what’s left.

What About if an EOT Decides to Sell A Small Portion of its Shares?

There will be situations where an EOT decides to sell some of its shares. Or, perhaps more likely, the trading company issues new shares which dilutes the EOT’s holding, without it being a full business sale.

This could be for a couple of reasons.

Reason #1: Incentivising Key Individuals

One reasonably common situation would be specifically incentivising a few key employees. For example, a business may want to offer share options to senior management.

This would enable them to agree on a share price today, where they can buy the shares for that price in a few years’ time.

The theory here is that this incentivises the staff in question to push the business to grow, so they can then buy the shares at a bargain price.

Any such share options are typically lost if the person leaves employment with the firm, so it also encourages them to stay. A carrot dangled in the future to tie them to the business.

Doing this will dilute the EOT’s shareholding. However, it may be a reasonable argument that it’s actually for the benefit of the majority of employees to incentivise these key people to put their all into the company.

Better to have 90% of a huge pie than 100% of a small one!

Reason #2: Receiving Financial Investment

John Lewis has recently been in the news (April 2023) as they’re considering possibly taking investment in return for a minority stake in the business.

At the time of writing, John Lewis is 100% EOT owned.

It’s generally been covered in the press in a negative light that they’re considering diluting this. Apparently it’s proof that employee ownership doesn’t work!

In reality, the retail sector has been having a horrible time for the last decade or two. Many similar, privately owned retailers have gone bust during that time, whilst John Lewis is still standing.

Some within John Lewis are of the view that they need a big cash investment to push the business forward.

Again the logic is that it’s better to have 90% of a big pie than 100% of a smaller one.

Key thing with either of these is that the EOT isn’t reduced below having a controlling stake in the company. If it did, it would no longer qualify for things like £3,600 annual tax free profit share payments.

Generally in these situations the tax impact would be far less significant. Reason being the company is raising investment which it then keeps, rather than selling the business and handing the net proceeds to employees.

Summary

Strictly speaking, an EOT cannot be sold, but it can sell its shares to a third party.

As EOTs are a fairly new concept in the UK, this is something that has rarely happened so far. Plus some who have been tempted and looked into it may have been put off by the harsh tax consequences.

Out of the lump sum received for selling the shares, CGT will be payable, along with any deferred consideration to the original owner.

Benefitting employees will also have to pay income tax and National Insurance contributions on any money left, as they receive it as a cash bonus.

The end result is what initially might seem like a golden egg, is actually rather less appealing.

On top of this, it will take the agreement by the trustees that it’s in the best interests of the majority of employees. Is a short-term cash receipt really better than the (hopefully positive) status quo?

Plus these same staff will be aware that doing that will forego their right to future profit shares and that they are handing over control of their company to a third party.