On this page

- An EOT is an exit plan

- What happens to the company leadership?

- What is a trust?

- How are decisions made in an EOT?

- How much do I sell for?

- How do I get paid for my shares?

- How much do staff pay for shares?

- How are profits split up?

- Does the EOT have to own all the shares?

- How does the tax work?

- What are the criteria to qualify for the tax perks?

- How many staff does the company need?

- Which business are most suited to employee ownership?

- Want to learn more about EOTs?

- Read more

The business owner sells a controlling interest of the company’s shares to an Employee Ownership Trust (EOT), rather than to a third party or through a management buyout.

As the EOT has no money, it repays its debt to the previous owner using company profits over an agreed period. During this period, staff can still benefit financially, should there be excess profits.

Once the debt is cleared, employees become the sole beneficiaries of the EOT and enjoy financial benefits in the form of profit-sharing payments.

Thinking about an EOT? We'll help you work out the right next step.

Book my free video call with Chris

We always respond within 24 hours.

An EOT is an exit plan

It’s critical you understand you’d be selling a controlling stake in your company to the trust. You can still work for the company, and potentially retain a minority stake, but it won’t be “your” company anymore. If you’re not at peace with that, you’re not ready for an EOT sale.

Often, founders will stay around for a while post sale, continuing to work for the business in some capacity. There are no rules on this, or even “norms”, it will vary significantly from company to company. But founders must be aware they’ll no longer be invincible, and can be outvoted on business decisions.

What happens to the company leadership?

Most small business owners are both shareholders and directors of the company. They therefore don’t distinguish between what they do/receive in their capacity as shareholder vs director. Selling to an EOT changes all that, as the majority shareholder will now be a trust, but the directors will still be one/some individual(s) working for the company.

It’s worth stressing leadership doesn’t have to change, at least not at the same time as the EOT sale. The EOT sale itself is a change, which can cause some concern/confusion. Hence care should be taken if you’re changing company leadership at the same time, to avoid rocking the boat too much.

What is a trust?

It’s a vehicle set up to own an asset, typically used where you want to separate the beneficial owners from the people who control it.

For EOTs, the beneficial owners are the employees. If the company makes big profits, the employees get to enjoy them. If the EOT goes on to sell the business, the proceeds will go to the employees (though this raises its own issues).

How are decisions made in an EOT?

For the trading company itself, decisions will continue to be made by the directors/senior team. However, above them, there are now trustees (who replace shareholders). So who are the trustees?

For small businesses we recommend you start with three trustees as a practical minimum. Here’s why:

- One trustee would control the company. This goes against the ethos of an EOT (no one person should have control).

- Two trustees would run the risk of deadlock if they can’t agree on a decision. In theory you could give one trustee the casting vote, but this gives one trustee full control.

- Three trustees removes the possibility of deadlock and of one person holding more sway.

When deciding who should be trustees, we think this is a good starting point:

- Director trustee – often this will initially be the founder. They should have good knowledge of the business strategy and finances.

- Employee trustee – ideally not someone very senior. They should have good knowledge of how the staff are feeling/what’s important to them.

- Independent trustee – often a business adviser or accountant. They should be external to the business, but care about it, and offer impartial wisdom.

How much do I sell for?

Your company needs to be independently valued. This valuation will then form the upper limit of what you can sell for.

It’s worth bearing in mind that a higher sale price isn’t necessarily better. Whilst the staff will have negligible involvement in negotiating the price, and won’t pay anything themselves, you will be relying on their efforts over multiple years to make it work and pay the sale price.

If the deal is set up with a top end price, so most profits will go to you for many years, there’s not much in it for the staff. If they can’t see a positive future for themselves there, they can just go and work elsewhere. If several key staff do that, the business can quickly fall apart, along with the payments to you.

Read our cautionary tale about Greedy Greg to see how this could play out.

How do I get paid for my shares?

You sell your shares to a trust. As the trust will be newly created, it won’t have any of its own money. But it will own the shares in the trading company. This means it’s entitled to receive distributions out of the trading company’s profits.

If you’ve been squirreling away funds for a while, your company may have a hefty war chest. If that’s the case, great, this can form a day one payment to you. You’ll then typically be paid the remainder over several years from future profits.

Find out more about funding an EOT

How much do staff pay for shares?

If we’re just talking about the EOT, then nothing. It’s important your staff understand they’re not buying anything as an individual, and won’t own anything personally. The plus side is they can benefit without putting any money in, so they’re not risking any of their own money. But in turn it means they won’t own anything that they as individuals can sell or take with them if they leave the company.

How are profits split up?

As part of the sale, a payment plan will be agreed for the trust to pay for your shares. Typically this will mean you’ll get any excess retained profits, and a chunk of profits going forward for an agreed period. In practice, this may mean profit share payments to staff will be modest for a while post sale.

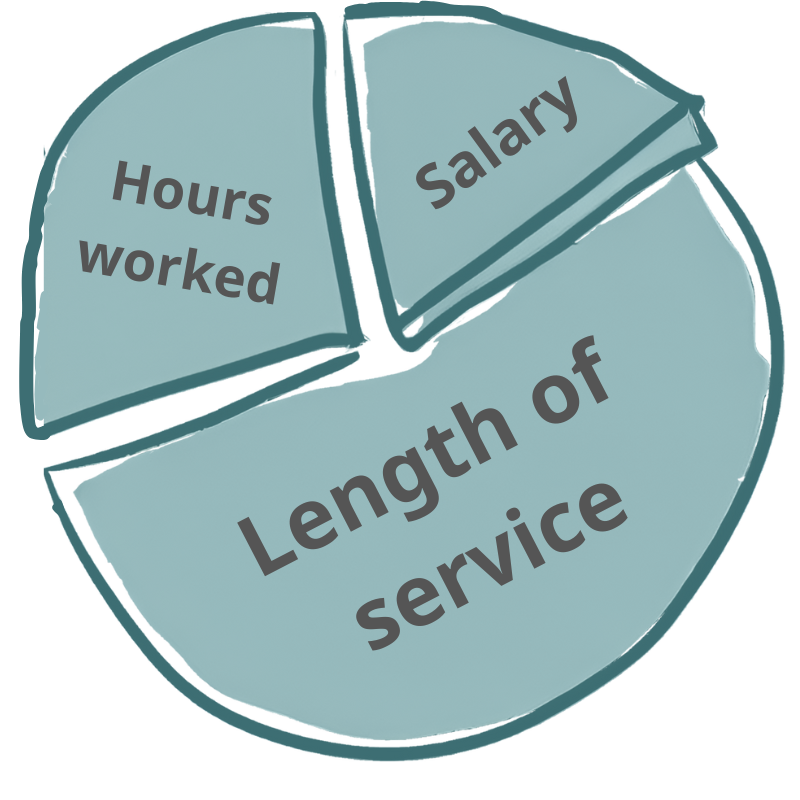

Where profit share payments are made to staff, you can choose from a range of options. It can be shared equally so everyone gets the same, or it can be split in line with different factors:

- Salary – higher paid staff get proportionally more

- Length of service – longer serving staff get proportionally more

- Hours worked – part-time staff get less than full time staff

The key thing is these are not performance based. Star performers can’t be specifically rewarded with higher share of profits. Similarly poor performers can’t be punished with lower share.

Does the EOT have to own all the shares?

No, it doesn’t. It does need to acquire, and retain, a controlling stake. But that potentially leaves up to 49% of the company’s shares up for grabs by individuals.

Sometimes founders want to retain a stake. Sometimes it’ll make sense to issue share options to senior employees. This can give them greater incentive to really push the business to do well, and do whatever it takes to keep the business afloat when things are tough.

But the simplest situation is the EOT buying 100%, and retaining 100%. It minimises risk of mixed motivations, and causes as little “us vs them” as possible.

How does the tax work?

Selling to an EOT offers a tax efficient way to exit your business. Put simply, if you meet the criteria, expect to pay just under 12% effective Capital Gains Tax on the sale price. Strictly speaking you pay CGT on half the sale proceeds, at your main CGT rate, typically 24%. The remaining half you may hear is “tax free”. It's technically a “nil gain nil loss” transfer. In practice this does mean it's tax free for the vendor, but the gain then sits in the trust, to crystalise if/when the trust sells the company on further down the line.

The other main tax perk is employees can receive £3,600 of tax-free profit share payments each tax year. It worth stressing they’re tax free, but not NIC free. It's also worth stressing (for particularly profitable firms) that the £3,600 isn’t an upper limit on profit share payments, it’s just the amount that can be tax free. So if a company makes £1million profit and has 10 employees, they can potentially receive £100,000 profit share each!

What are the criteria to qualify for the tax perks?

- The company being sold to the EOT needs to be a trading company, or the holding company of a trading group.

- The EOT needs to gain a controlling stake – at least 51% (there can’t be any funny voting rights that somehow enable you to keep control).

- Staff profit share payments need to be equitable. We’ve detailed some of the options for this above. The key point is that you can’t single out individuals positively/negatively, so it can’t be a performance-based bonus.

- The participator ratio. This one initially sounds straight forward, but can easily get very complicated. Oversimplifying, you need at least 5 employees for every 2 shareholders.

How many staff does the company need?

From a box ticking legal perspective, the participator ratio is key. Oversimplifying it a bit, you need at least five employees for every two shareholders. So in theory, a company that’s 100% owned by one person would just need two other employees (in addition to the founder) to qualify.

But the business also needs to continue operating successfully for multiple years. Which is why this model is well suited to stable, profitable businesses, with a competent team.

Which business are most suited to employee ownership?

The short answer is if your business fits the criteria listed above, employee ownership is a viable option. There are no industry-specific barriers to a business become a successful EO enterprise. In fact, EOTs are increasingly found in all major sectors of the economy and in every region of the UK. From companies with just half a dozen employees, to household names like John Lewis and Ardman Animations.

Want to learn more about EOTs?

Our free 10 EOT Essentials handbook covers the key things every founder should understand before selling to an EOT. From payment plans to profit sharing, business suitability to trustee boards, it deals with the technical, the psychological and the practical.