It can be tricky to get your head round how the finances work in an EOT sale.

You’ll hear things like:

- founder gets paid fair market value for their shares

- nobody (including staff) puts any money in

- taff gain benefit of future profits

How can all these things be possible?

The short answer is, for a while after sale, staff profit share bonuses are often modest, as much of the profit goes to the founder.

How finances work in an EOT transfer

Below we give example finances of an imaginary, but fairly typical, Go EO client: the situation before EOT sale, and the situation after, with details of who gets what at each point.

Company figures pre Employee Ownership Trust

Company figures pre Employee Ownership Trust

- Joe Bloggs owns 100% of Example Ltd

- It has 10 employees

- He wants a 100% sale to an EOT

Let’s look at the business finances:

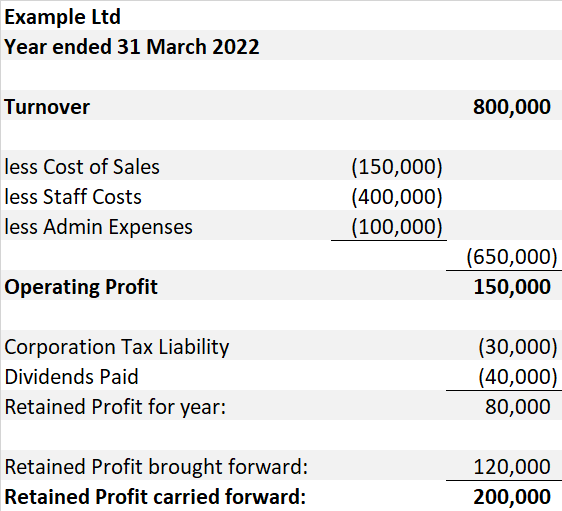

Profit and loss (year before sale)

It’s been profitable for a few years.

As a service-based business, biggest costs are staff, at 50% of turnover.

Other costs aren’t trivial, but still leave a circa 20% net profit.

Joe stopped withdrawing all profits a few years ago. Restricting his total personal earnings to ~£50k/year.

This gave the company a nice buffer. It also kept his personal tax bills modest as he’s been planning for an EOT for some time.

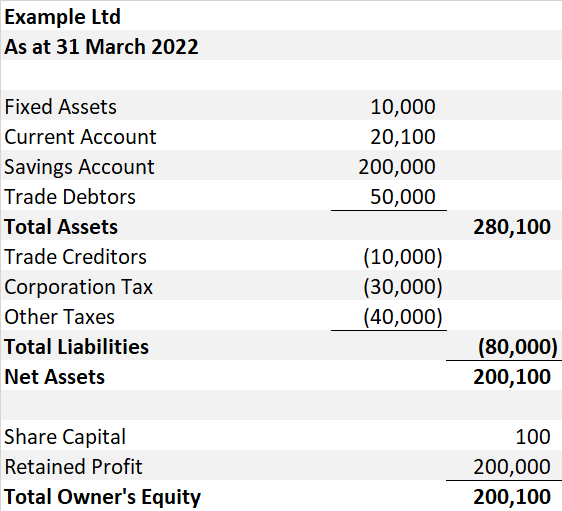

Balance sheet (immediately before sale)

The company has £200k cash in savings. This is far more than is required as working capital, well above the liabilities.

£200k is more than the company needs. Joe’s been planning the EOT transfer for a while, so built a cash pot to make a healthy initial payment to him.

Other items on the balance sheet are standard, nothing out of the ordinary.

The company’s credit control is good. Trade debtors all new, no bad debt concern.

Valuation

The company is independently valued. Valuations are typically based on an “adjusted EBITDA multiple“.

What is EBITDA?!

Earnings Before Interest, Tax, Depreciation, and Amortisation.

For most small straight forward businesses, EBITDA will be similar to the company’s “Operating Profit” (before corporation tax).

In the case of Example Ltd, there would have been depreciation on the fixed assets. But it’s trivial enough we can ignore, so EBITDA is £150,000.

Why “adjusted” EBITDA?

Small owner managed companies rarely pay founders big salaries. Owners normally pay themselves an NIC threshold salary (currently ~£9k/year), with most of their remuneration as dividends. Whilst this can be more tax efficient, it causes a problem here.

The EBITDA figure above is after salaries, but before dividends.

Is £9k/year fair payment for Joe? If he stepped away, could the business replace him for £9k/year? Probably not!

Going forward, Joe won’t own shares, so won’t receive dividends. We should adjust EBITDA to what it would be with fair market salary for Joe.

In this case, Joe’s winding down, works part time. It’s agreed £39k would be fair market value, £30k higher.

This gives an adjusted EBITDA of £120,000.

What multiple to use?

There’s no one correct number here. A few things will be considered:

- Any industry norms?

- Is the business growing, stable, or in decline?

- Recurring revenue is more valuable (as more reliable) than project income.

- Does the business have any unique distinguishing features competitors can’t copy?

- Consider opportunities/threats on the horizon. Expectation of significantly increased/decreased profits?

Some businesses may have intellectual property, or other assets making them valuable. However, these things may be ignored in an EOT sale. Reason being the founder can only be paid out of profit. Hence whilst some promising intellectual property that may lead to profits in 5+ years could appeal to exernal investors, it’s of limited help to an EOT sale.

Often a multiple of 3 to 4 is reasonable for an EOT sale.

Valuation of Example Ltd

With £120k adjusted EBITDA, multiple of 4, profitability suggests a value of £480k.

But there’s £200k net assets in the company at time of sale, should that be added?

Sort of. £200k cash in a company bank account is worth less than £200k in a personal bank account, primarily due to tax.

We agree £120k could be justifiably added to the valuation for balance sheet value, giving a total value of £600k.

EOT payment plan

We’ve agreed Joe’s owed £600k for his shares. How and when does he get it?

Up-front payment?

The company has net assets of ~£200k, including £200k in savings. This could all come out to Joe as an up-front payment.

But the senior team are nervous paying it all out. What if some of those trade debtors failed to pay on time? The business might struggle to pay creditors when they fall due.

It’s agreed the company will pay Joe £150k from savings immediately. Great!

- he gets £150k tax free now

- company still has healthy £50k buffer

- now £450k to pay going forwards

Future payments?

The company’s adjusted EBITDA as calculated above is £120k/year.

Joe is aware he’s expecting significant capital payments. He’s happy to continue working the same amount as he was before, on just his £9k/year salary.

Going for a higher salary would reduce the company’s profits. It would take longer to pay him off, and/or reduce profit share to staff. He’s happy he’s doing very well from the deal, especially with the tax perks.

Given he doesn’t ask for any extra salary, we can plan based on the non-adjusted EBITDA, so £150k.

Remember capital payments to the founder will be from post corporation tax profits. So the most the company could pay per year would be £120k (with 20% tax rate). This assumes the business profits remained consistent.

(click to see our separate blog post re EOT funding)

What does the founder get?

With the above plan, Joe gets:

- £150k up-front payment, tax free

- £60k/year payment, tax free (for 7.5 years)

- £9k/year salary, for as long as he/the senior team deem it appropriate

So Joe gets £150k, then £69k/year in total from the company going forwards. There’ll be zero tax/NICs to pay (remember the “income” part is only £9k). This should last 7.5 years.

After that, Joe may continue to work there, but would only be due fair market salary (plus profit share like other staff).

But…

He’s handed over control and future profits of the company. It’s no longer “his” company.

If the business fails within 7.5 years of transfer, Joe won’t get all £450k. If it fails quickly, he may get little beyond the initial £150k payment.

On the flip side, the team may do an amazing job. Building the business to 10 times what it was. Joe won’t benefit financially from that.

7.5 years post transfer, Joe owns nothing. He may still work for Example Ltd, but zero capital payments, zero dividends. He’s “just” an employee, no different to any other.

What do the staff get?

They inherit a company with £50k net assets, £150k/year profit, less £60k/year (post corporation tax) to Joe for 7.5 years. No staff member pays anything for this.

What can staff expect?

- their salary, as before

- profit share. Forecasts suggest £60k-75k/year. With 10 employees, averages £6k-7.5k/employee/year. And £3.6k of it is tax free.

- In 7.5 years Joe should be paid off. Will leave an extra £75k/year (before corporation tax). I.e. £150k total/year available for profit share.

Plus they’ll have power to make changes in how the business is run.

Financially, there’s no downsides for staff.

There’s no risk of staff losing money due to the EOT. If the business fails, they are out of a job. But this is no worse than pre EOT.

The senior team may have more responsibility. The buck stops with them. Not everyone wants this, so consult senior staff before transfer.

- some may want to stay “followers” rather than become “leaders”.

- consider salary increases for those who lead.

The only other potential downside on financial front is if staff had expectations (realistic or deluded!) of receiving shares personally.

Company figures post Employee Ownership Trust

- Joe Bloggs now owns 0% of Example Ltd

- It still has 10 employees

- Profits to be split for 7.5 years

Let’s look at the business finances now, key changes highlighted:

Balance sheet (immediately after sale)

Not much change here. Remember, it’s the company’s ownership that’s changed. Little has changed with the company itself.

It’s gifted £150k savings to the EOT, which in turn uses them to pay down the debt to the founder.

From the company’s perspective it’s as if it paid a large dividend. Retained profits and cash reduced, no other balance sheet impact.

There will likely be some professional fees, plus £3k stamp duty associated with the purchase, not reflected here.

Profit and loss (year after sale)

Turnover and costs same as year before.

Directors agree a £75k profit share payment to staff. This goes via payroll, reducing taxable profit, hence corporation tax.

They had to set aside enough post CT profit to make the deferred consideration payments.

The figures chosen:

- Met obligations to creditors/founder

- Gave employees a nice bonus

- Still £50k retained as buffer

This seemed a good balance. All parties happy, minimal risk for the business.

Is this always how it works?

About 1,000 UK companies have transitioned to EOTs in the last decade.

Individual circumstances will vary. Some deals will have more “0”s on the end of the numbers! But they’ll have followed a similar route to the above.

The variations in transactions can be significant.

- Valuations big and small

- Founders giving away vs selling for full market value

- Short vs long payment plans

These all cause who gets what, and when, to vary massively.

Some EOT transfers are amazingly generous to the employees (whether they appreciate that or not is another matter!).

Other EOT transfers will involve the founder maximising their return. Staff then have to work hard for ages just to pay the founder off.

We’re in favour of a balanced transaction. The founder deserves reasonable reward, but paying it off must be comfortable for the business/staff.

(See our cautionary tales of founders Greedy Greg and Generous Jenny, two extremes, both end badly!)

How Go EO can help

Go EO will discuss your situation with you.

- How do your company’s finances stack up?

- How generous do you want to be to staff?

- What’s a tax efficient way of achieving it?

Considering this for your business? Get in touch!

Summary

With the financials of a company transferring to EOT, the key things are:

- Profit multiple indicates business value

- Healthy balance sheet may enable up-front payment

- Payment plan will suggest when remainder is paid

- Founder cashes in, gives up long term rewards

- Minimal downside to staff, but upside may be delayed

Hopefully the above helps you understand how the finances can work.