One of the most commonly asked questions when it comes to employee-owned businesses is what happens to the profits in an EOT.

Whilst EOTs will have varying levels of profit depending upon the size and nature of the company, the way they will distribute them is usually fairly similar.

And that is what we are going to look at in today’s blog.

So without further ado, let’s get started.

What Happens To The Profits In An EOT?

The distribution of profits in an EOT will be approved by the directors of the EOT company (known informally as “the trustees”), and can usually be sorted into four distinct categories:

1) They Are Used to Pay Off the Founder

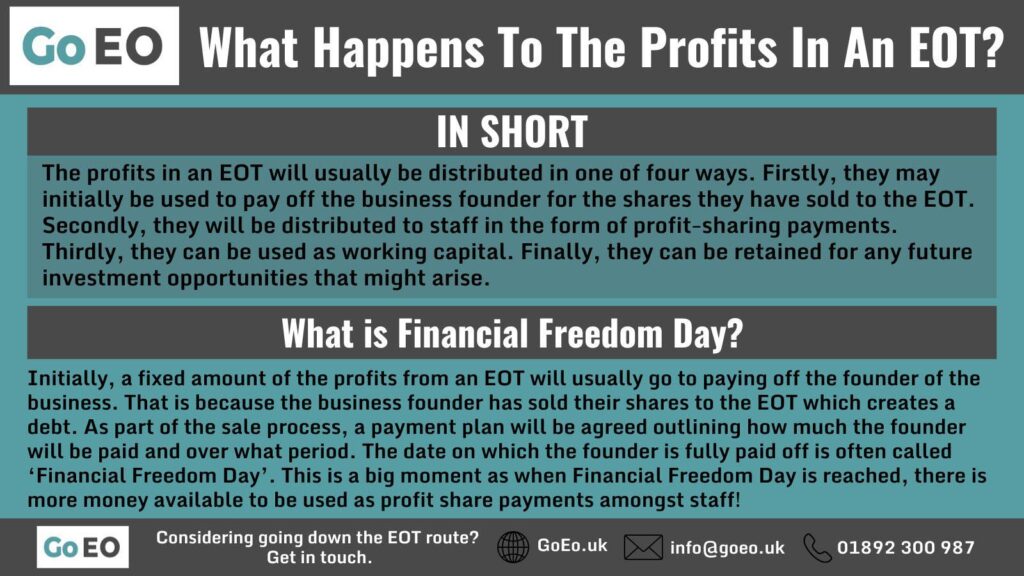

Initially, a fixed amount of the profits from an EOT will usually go to paying off the founder of the business.

That is because the business founder has sold their shares to the EOT which creates a debt. This debt will be paid off over time from the future profits of the business.

As part of the sale process, a payment plan will be agreed outlining how much the founder will be paid and over what period.

The date on which the founder is fully paid off is often called ‘Financial Freedom Day’.

This is a big moment as when Financial Freedom Day is reached, there is more money available to be used as profit share payments amongst staff!

It should be noted that this doesn’t mean staff can’t benefit from profit-share payments whilst the founder is being paid off. They still can, and we go into more detail on this in the section below

In some instances, if the business founder needs to be paid off more urgently third-party financing may be arranged.

But usually, they will be paid off from future profits. This amount, agreed upon sale, paid gradually typically over multiple years, is known as the deferred consideration.

2) They Are Used as Profit Share Payments for Employees

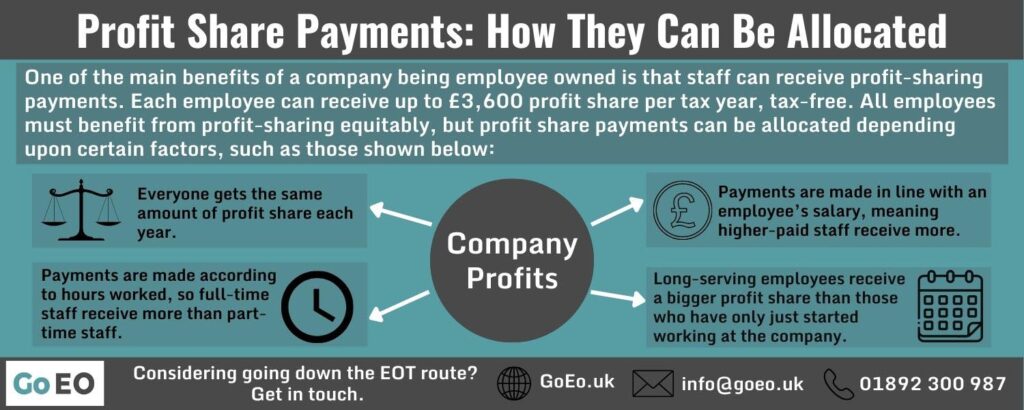

One of the main benefits of a company being employee owned is that the staff can receive profit-sharing payments.

And each employee can receive up to £3,600 profit share per tax year, tax-free. Anything above that will be taxable in the way a normal salary is. Profit share payments are still subject to National Insurance contributions as well as other factors like student loan repayments, but income tax does not apply to the first £3,600 of profit share payments per tax year.

Another perk is that this is all dealt with directly by payroll, so there is no additional admin for individual staff members to deal with such as including it on their own personal tax return for instance.

But let’s quickly recap on the point we made in the section above, the fact that even if the business founder is still being paid off for his share of the profits, staff can still receive profit share payments at this time.

A lot of this depends upon the payment plan that has been agreed upon for the founder, and what happens to profit levels in the business after sale.

If the founder has agreed to be paid off over a long period, with smaller payment instalments, and/or the business thrives soon after sale, then staff will most likely receive modest profit share payments during this period.

If the founder has gone for the opposite option and agreed to be paid off over a short time frame, and/or business profits fall after the sale, staff might not receive any profit share payments.

However, with higher payments to the founder, they’ll be paid off more quickly, and once Financial Freedom Day comes staff will go from having little or nothing in the way of profit shares, to potentially having a lot!

Think of it a little like the mortgage on a home. Some people will choose to pay it over a prolonged period of time, accepting the fact it will take longer to pay off, but enabling them to benefit from more spare cash to use now. Others will want to clear that debt as soon as possible. Doing so will mean little disposable income in the short term, but of course the debt will be fully paid off sooner.

It should also be noted that all employees must benefit from profit-sharing equitably.

However, this doesn’t necessarily mean that every employee has to receive the same amount of profit share at the end of each year.

The trustees can decide to allocate profit share payments depending upon certain factors, for instance:

- Everyone could get the same.

- Payments could be made in line with an employee’s salary, meaning higher-paid staff receive more.

- Long-serving employees could receive a bigger profit share than those who have only just started working at the company.

- Full-time staff could receive more than part-time staff.

But the EOT cannot skew the benefits of profit sharing to individual employees or groups of employees. Hence individual brilliant or poor performers cannot be singled out with particularly high or low-profit share payments.

Perhaps worth stressing that good performers can be individually rewarded with bonuses in the normal way (ie not EOT profit share payments). It’s purely the profit share that must follow an equitable route as outlined above.

3) They Are Used as Working Capital

Employee-owned businesses are no different from any other business in that they need working capital, which is essentially a buffer of cash to help the business run smoothly.

Working capital funds the day-to-day operations of the business, so it can meet any short-term financial obligations.

Sometimes businesses can have significant retained profits, without having much cash. For instance perhaps a lot of the company value is tied up in fixed assets, or stock, or even trade debtors who are slow to pay. Hence having profits doesn’t always mean physical profit share payments can be made to the staff.

Usually a business that becomes an EOT will have already been running for a while, so it should have a good element of stability, and be profitable.

Nevertheless, trustees will usually allocate a share of the profits as working capital.

4) They Are Retained for Future Investment Opportunities

The final way profits in an EOT can be used is by retaining them for any future investment opportunities that might arise.

This could be done in various ways, but the goal will be to improve the profitability, productivity and efficiency of the business.

And when invested correctly, the growth of the business will mean employees benefit from higher profit shares in the future.

Summary

So in summary, the profits in an EOT will usually be distributed in one of four ways:

- Initially, they will often be used to pay off the founder for the shares they have sold to the EOT. As part of the sale process, a payment plan will be outlined detailing how much the founder will be paid and over what period.

- Staff will receive them in the form of a profit-sharing payment each year. In the case of point 1 above, staff can still receive a profit-share payment each year even whilst the business owner is still being paid off.

- They will be used as working capital for the business.

- They will be retained and used for future investment opportunities to grow the business and increase profitability.

The trustees of the EOT will need to approve the distribution of the profits and this also includes how any profit-sharing payments to staff are allocated.

All profit-sharing payments must be distributed equitably, but they can be apportioned depending on certain factors, such as salary, length of service and hours worked, so long as individual employees of groups of employees are not favoured.

This is how profits are usually distributed in an EOT.