Acronyms can be confusing and mystifying at the best of times, and when it comes to business matters even more so!

With regards to employee ownership and share options in companies you might hear a number of terms used.

In today’s article, we are going to take a closer look at some of the most popular, what they are and how they compare to the EOT model.

So let’s start by looking at the main share options offered to employees by businesses.

What Is The Difference Between An EOT And EMI? (Or CSOP Or SIP)

What is an EMI?

An Enterprise Management Incentive (EMI) plan is a flexible and tax-efficient share option, designed to support small and medium-sized businesses recruit and retain employees and support their future growth.

The share option can be offered to all employees that spend at least 25 hours per week, or 75% of their working time working for the company.

There are a few qualifying conditions that enable a company to qualify for this, namely that it must not have gross assets in excess of £30million and it must have fewer than the equivalent of 250 full-time employees.

Also certain types of businesses are specifically excluded from qualifying for EMI. Examples are those in banking/insurance, legal/accounting, property development, farming, plus a few other niche industries. See here for a full list.

EMI share options work in the same way as many other share options. That is an employee is granted an option over a specific number of shares in the company, at a set price at some point in the future.

The tax benefits are very appealing, with no income tax or NI contributions payable on the grant of the option.

When the employee sells the shares, capital gains tax will be payable only on the difference between the sale proceeds and the market value of the shares when the option was granted.

What is a CSOP?

Like an EMI, a Company Share Option Plan (CSOP) is a share option scheme that has significant tax advantages.

Most notably it can be exercised without income tax or NI contributions dependent upon certain factors.

However unlike an EMI, when it comes to company size or number of employees there are no limits for a CSOP.

Also some of the trade restrictions that apply to EMI don’t apply to CSOP, so more companies qualify to use it.

But there are other restrictions that an EMI isn’t subject to, for instance:

- The share options must be granted at market value.

- Each employee can only be granted a maximum of £60,000 of options (the figure was £30,000 for any shares granted before 6 April 2023).

- Any gain is exempt from income tax only if the options are held for at least three years and within ten years of the grant date.

Many companies that do not qualify for EMI options due to their size or trade, may be able to use CSOP options.

Both EMI and CSOP tend to be used to help incentivise a small number of key staff.

What is a SIP?

A Share Incentive Plan (SIP) is tax-advantaged plan that allows companies to invite eligible employees to acquire fully paid, non-redeemable shares (as opposed to share options) in the company.

There is no requirement to agree a market value of the shares with HMRC before they are awarded, but HMRC must be notified of the SIP by 6 July of the following tax year.

The shares are held in an employee benefit trust, and as long as they are held for between three and five years, no Income Tax or National Insurance will be paid on their value.

No Capital Gains Tax will be payable either as long as the shares remain in the trust.

SIP shares can be gained in four ways:

- Free shares: The employer can give an employee up to £3,600 of free shares per tax year.

- Partnership shares: An employee can buy shares out of their salary before tax deductions. They are limited to spending either £1,800 or 10% of their income for the tax, whichever is lower.

- Matching shares: The employer can give an employee up to two free matching shares for each partnership share they buy.

- Dividend shares: Dividends received from the free, partnership or matching shares can be reinvested into further shares.

SIPs also tend to be favoured by larger, and often listed companies as they can be expensive to set up and administer.

Unlike EMI/CSOP, SIP schemes are offered to all staff.

How Is An EMI, CSOP or SIP Different from an EOT?

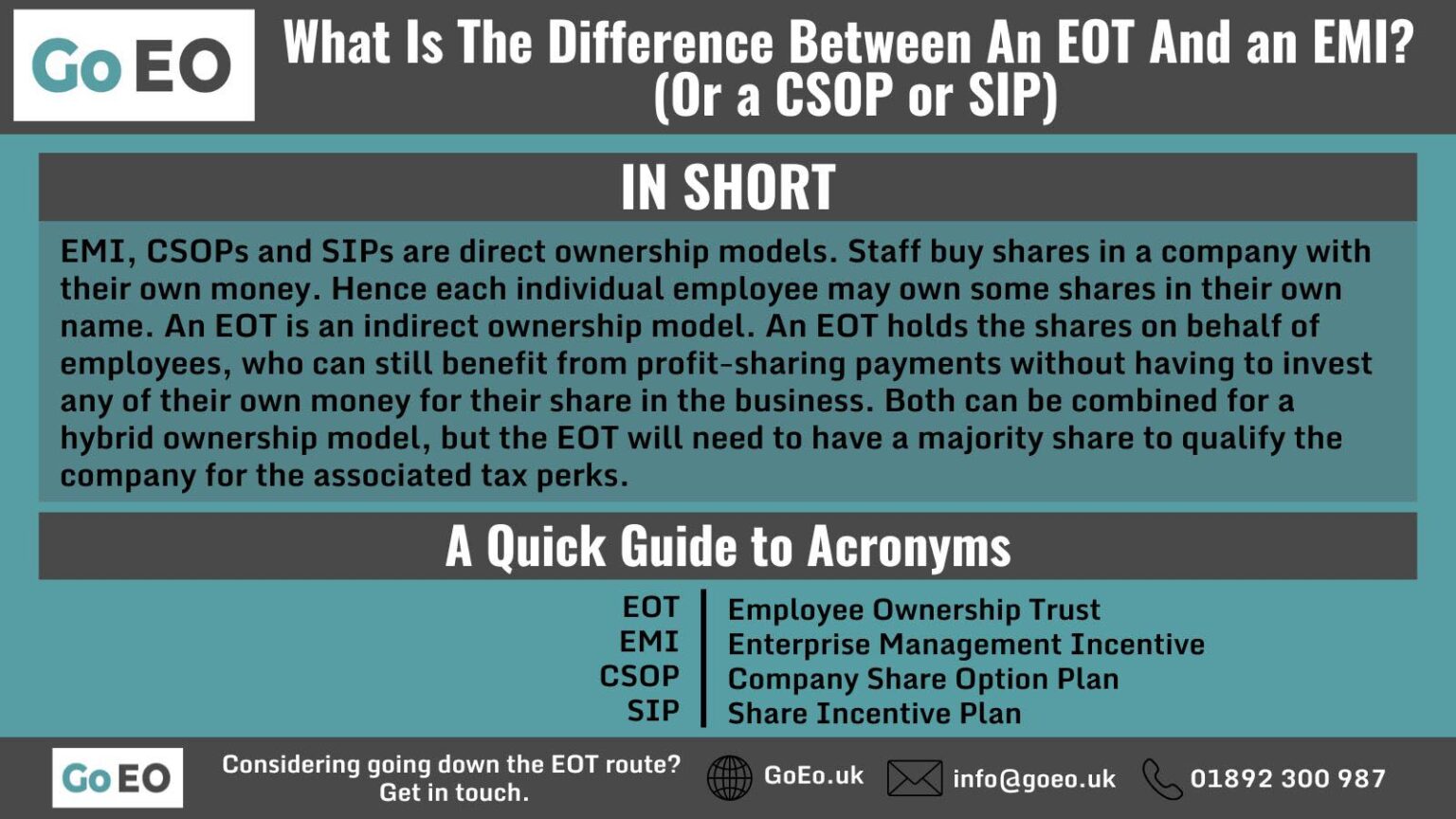

The simple difference between an Employee Ownership Trust (EOT) and the three other plans we have mentioned is that an EOT is an indirect ownership model, whereas an EMI, CSOP or SIP is a direct ownership model.

An EOT purchases shares from the selling business owner and holds them in a trust for the benefit of the trading company’s employees. The employees themselves never have direct ownership of the shares held by the trust.

So whilst you can’t see or touch the EOT, it’s the EOT that owns the shares in the company.

With an EMI, CSOP or SIP the employees invest their own money and own something of value they can sell later.

The acronym is just the scheme by which employees acquire shares. The employees will own shares in their own name.

Both indirect and direct ownership models have their own pros and cons, which we have covered in more depth in our blog looking at if it is good if a company is employee-owned.

Can You Combine Ownership Models?

There is no reason why you can’t mix and match an EOT structure with an EMI, CSOP and/or SIP, although the EOT will need to hold the majority of shares for it to benefit from the associated tax perks.

However, staff could still directly buy shares via any of the other options if they were available.

Sometimes an EOT may decide to sell a small percentage of its shares to either bring in new financial investment or to incentivise key employees to grow the business.

This is on the basis that the employees can buy shares at a bargain price, and then push the company to grow which will see the shares increase in value.

We looked at this more closely when we discussed if an EOT can be sold.

Summary

The difference between an EMI, CSOP and SIP, and an EOT is the fact that the first three are all ways staff can buy shares in a company directly.

That is they use their own money to buy the shares personally and can then sell them at a later date, or keep hold of them as a form of pension.

But when a business owner sells their shares in a business to an EOT, they remain with the trust.

The trust holds the shares on behalf of the employees, who are the beneficiaries of the shares, without ever actually owning them.

This means staff never have any shares they can sell personally, and when they leave the company they will no longer benefit, but also they do not have to invest any of their own money into buying shares and can still enjoy profit-sharing payments.

Some companies combine both direct and indirect ownership models, and as long as the EOT maintains a controlling stake in the company it still retains the various tax advantages such as the £3,600 annual tax-free profit share payments.