The basic concept of an EOT sale is that the money to pay for the sale comes from the business. But what does this look like in practice? Our example is based on a typical Go EO client: a profitable service-based business with 10 employees, looking to sell 100% of the shares to an EOT.

The scenario

- Business

- ABC Trading (10 employees)

- Current owner

- 100% owned by the founder

- Profit margin

- 20% net profit

- Valuation

- £600,000

-

Adjusted EBITDA: £120,000

Multiple: x4

Net assets: £120,000

Understanding our business valuations has more information on how this was calculated.

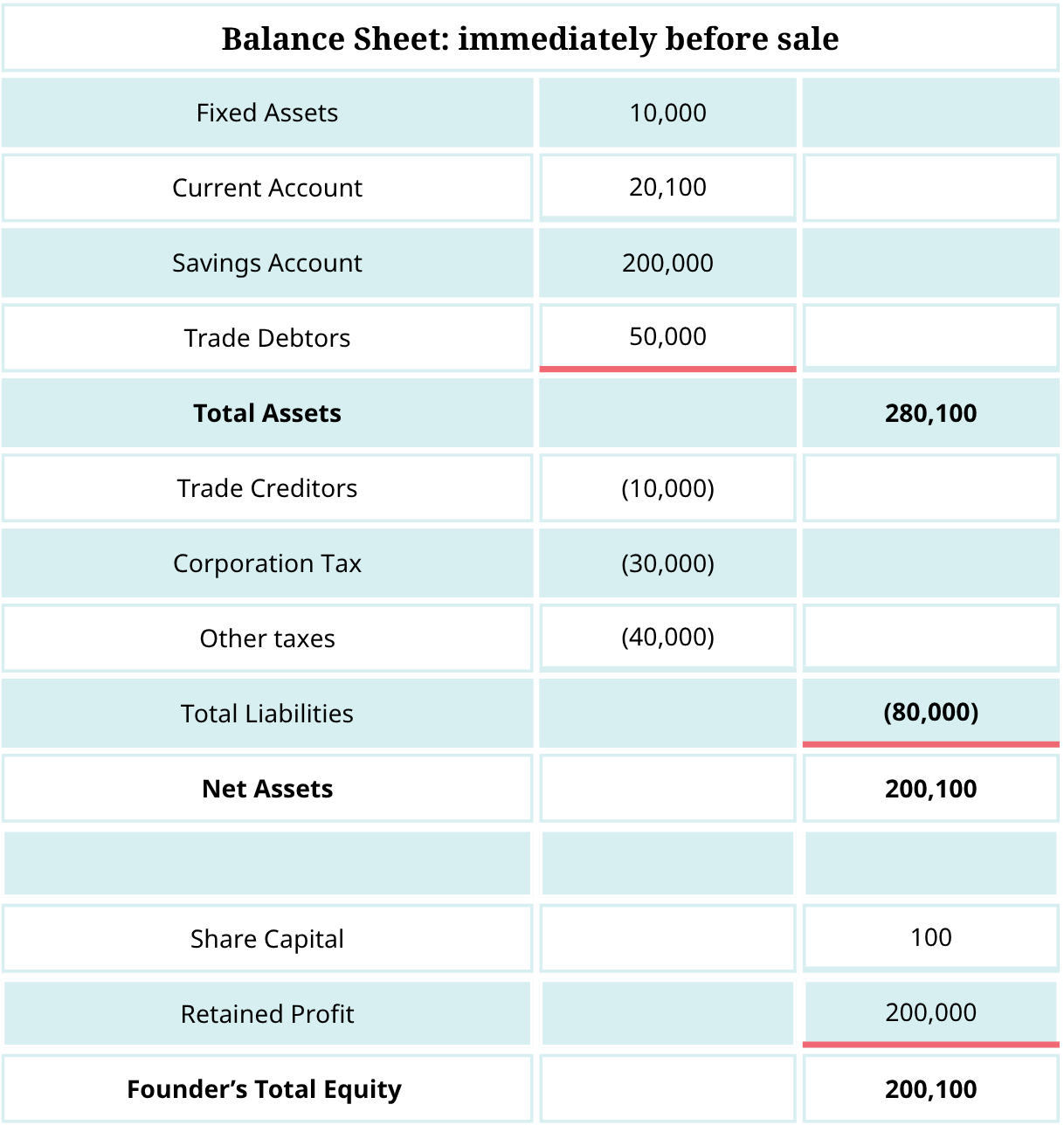

The balance sheet before the EOT sale shows total assets of £280,100 and founder’s equity of £200,100. The business is financially healthy, with significant savings that can be used as the initial payment to the founder.

Payment plan

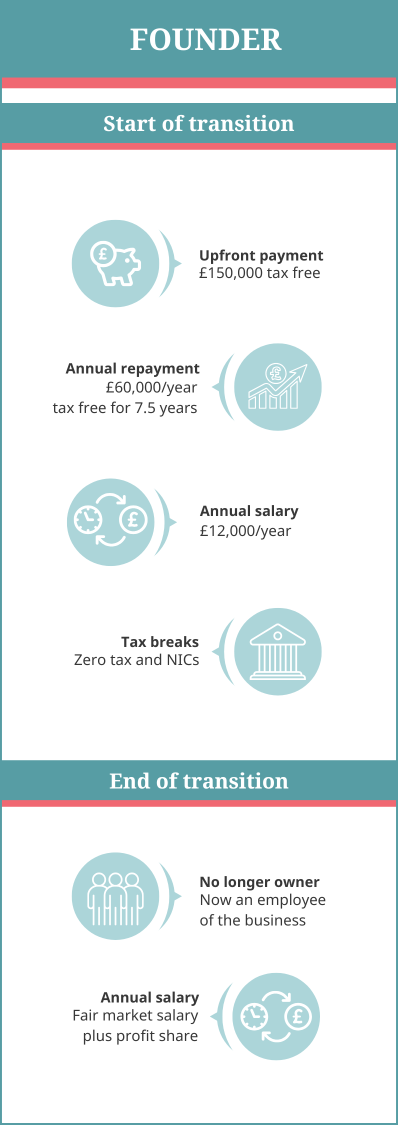

Upfront payment

Because the founder has restricted their personal earnings to £50,000 in recent years, ABC Trading has £200,000 in cash reserves. It’s agreed to pay £150,000 upfront, leaving a healthy buffer in the business to deal with any unforseen situations.

Deferred consideration

That leaves £450,000 to be paid over time from profits.

- Founder continues working for £12,000 salary

- Annual post-tax profits: ~£120,000

- Monthly payments: £5,000

- Total time to repay: 7.5 years

This leaves a buffer each year to fund staff profit share and cover any downturns.

What the founder and staff get from the EOT sale

How does this show on the balance sheet?

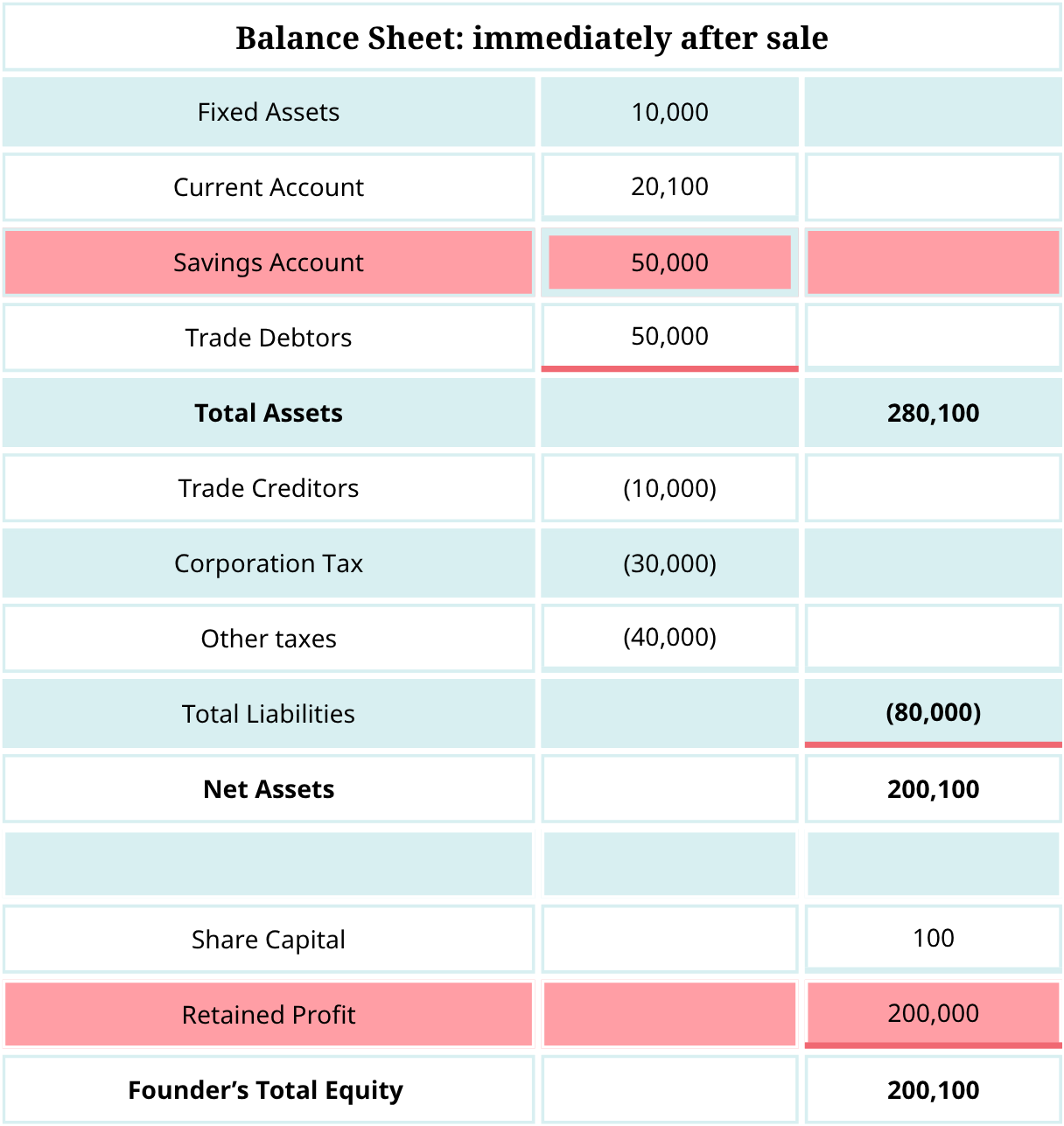

Even though the EOT now owns the business, the debt to the founder is legally owed by the EOT – not the trading company. The company’s balance sheet one-year post-sale looks largely unchanged. Some businesses choose to reflect the debt in management accounts to show progress on payments (like watching a mortgage balance drop over time), but if so, this should be removed for any formal statutory accounts.

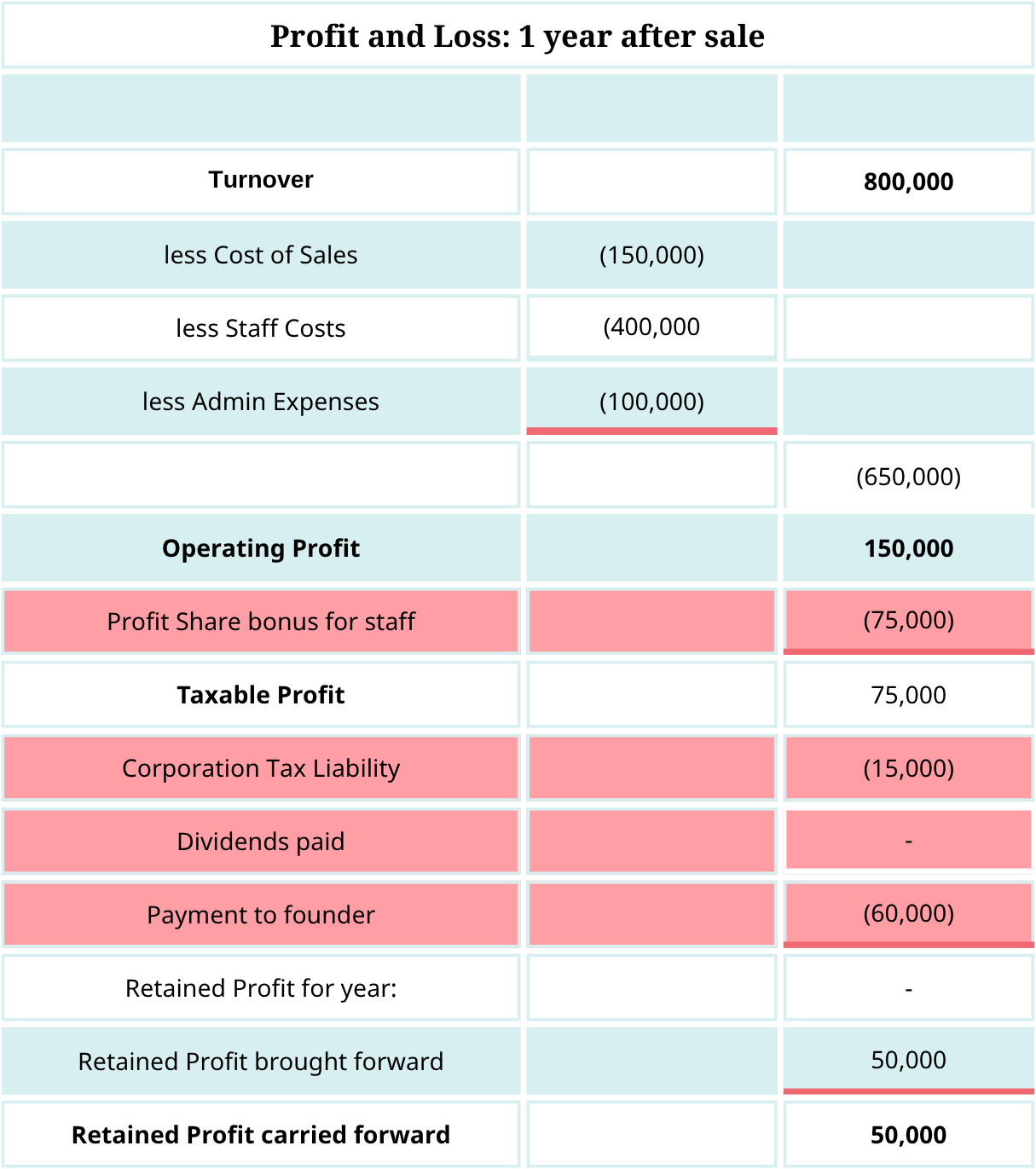

Profit & Loss: pre and post-sale

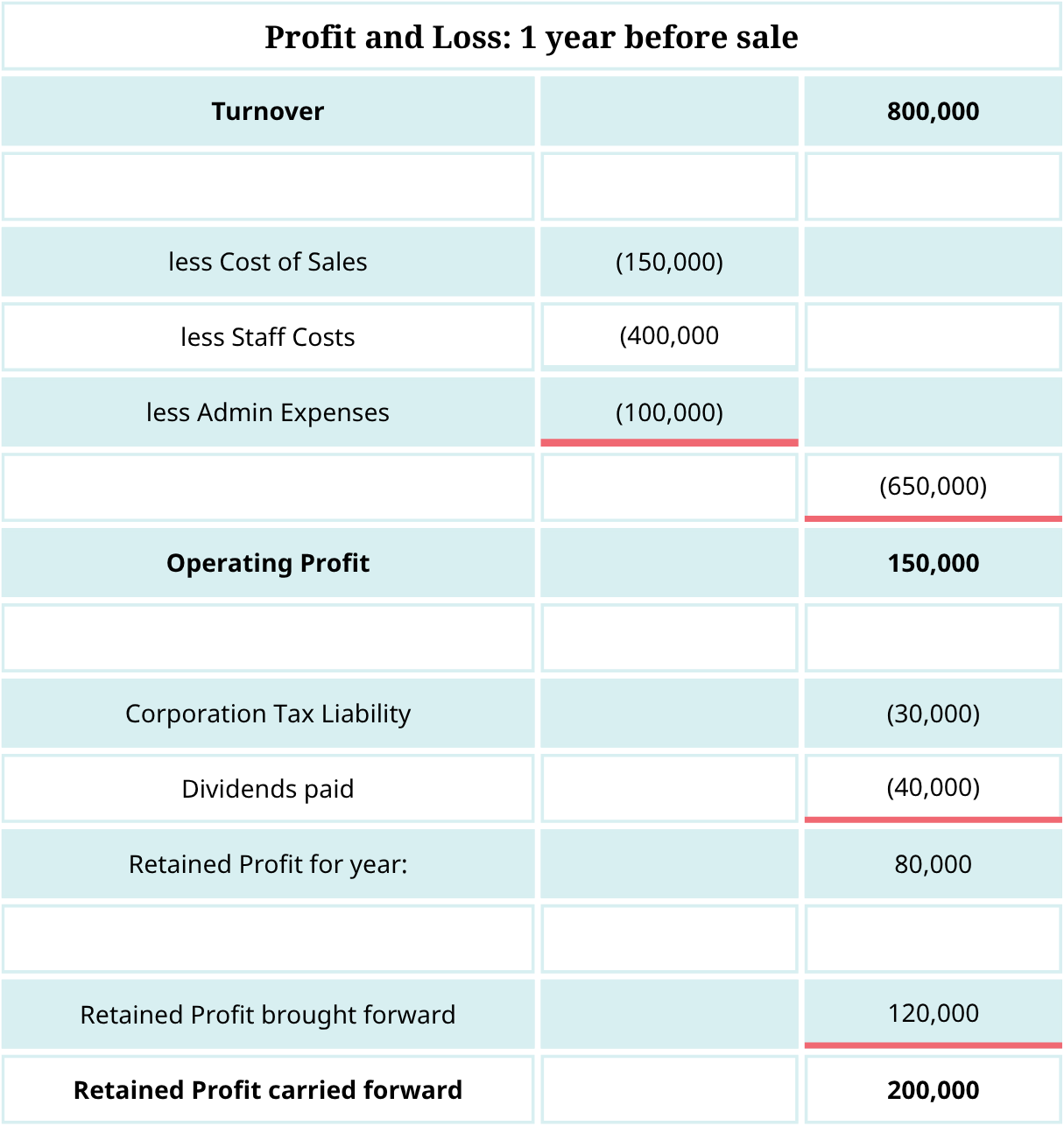

Pre-sale profit and loss show £40,000 dividend and £80,000 retained profit. Post-sale profit & loss showing £75k profit share, £60k payment to founder, and £50k retained profit. You can clearly see the shift in how profits are used: none going to the founder as dividends, more going to staff and EOT repayments post-sale. The company shares a significant profit bonus with staff while still making repayments and retaining a buffer.

How EOT-related payments work

The EOT owns most of the shares in the trading company and is entitled to most of the profits. But in practice, the EOT is a pass-through vehicle. It has no need to hold any money. It has no need for a bank account. Both up front and deferred consideration payments to the founder are made by the trading company on the EOT’s behalf.

EOT-related payments to staff work differently to the payments to the founder. Again, the trading company, not the EOT, will make the physical payments. However, unlike payments to the founder, profit share payments come from pre-corporation tax profits and are made via payroll. This is the reason EOT companies often have modest corporation tax liabilities. When they make profits, they pay the staff more, leaving minimal profits to suffer corporation tax.

Up to £3,600 of the profit share, per tax year, per employee is free from income tax, but it does suffer NICs. The trading company processes the payment in the same way as the salaries, and the employees receive the net salary amount.

A balanced and sustainable pathway

This example shows how an EOT sale can be structured to benefit everyone: the founder gets a fair value over time, staff begin sharing in profits early on, and the business stays financially stable.